Ипотечная ставка цб рф на сегодня: Банк России принял решение снизить ключевую ставку на 100 б.п., до 4,50% годовых

Жилье в ипотеку сегодня берут многие граждане России. Эта практика пришла к нам с Америки, Европы неслучайно: для миллионов наших граждан это единственная возможность перебраться с арендованной квартиры в собственную. Сложная экономическая ситуация в стране в 2018 г. привела к тому, что Центробанк решил принять меры, направленные на обеспечение устойчивого развития ипотечных предложений.

С 1 января 2019 г. в РФ начало действовать новое правило – по ипотекам с первоначальным взносом меньше 20% теперь будет повышен коэффициент риска со 150 до 200%.

Новые требования ЦБ по ипотеке в России

Почему Центробанк, во главе с председателем Эльвирой Набиуллиной, решил изменить правила ипотечного кредитования в 2019 году? Специалисты главного банка страны отметили, что ежегодно растет количество тех ипотечных займов, где первый взнос меньше 20%. Если тенденция и дальше бы сохранилась, то мог наступить дефолт.

Новое решение начало действовать с начала 2019 г., а распространяться оно будет на те виды ипотек, которые будут выданы с начала 2019 г. Из-за увеличения коэффициента риска теперь россиянам сложнее будет получить ипотеку. Увеличение этого показателя сразу на 50% вынудит кредитные организации создавать повышенные резервы под те ипотеки, одним из условий которых являлась выплата первого взноса в размере меньше 20%.

Комплексный подход к ипотеке в России

В 2018 г. в РФ начался рост инфляции из-за роста тарифов на ЖКХ, акцизов, налогов, НДС, сложной экономической ситуации в стране, вызванной наличием финансовых ограничений. Поэтому в 2019 г. ключевая ставка ЦБ выросла, а за ней начали расти и остальные ставки, в том числе и по ипотеке. В 2018 г. российские банки вынуждены были поднять свои ставки до значения 9,5% из-за того, что Центробанк два раза поднимал ключевую ставку – вначале с 7,25 до 7,5%, а потом и до 7,75%.

Несмотря на то что коэффициент риска был увеличен, процент по ипотеке тоже повысился на несколько позиций, специалисты считают, что Центробанк действует в правильном направлении. Он стремится минимизировать риски банков и людей по выплате ипотечной задолженности.

В 2019 г. главный банк страны рассматривает такие позиции, изменения по части ипотечного кредитования:

- Внедрение услуг по реструктуризации ипотеки, если заемщик потеряет работу;

- Применение накопительных касс для выплаты долга. Вначале заемщик накапливает деньги на индивидуальном счете в банке, а затем определенная сумма может быть использована вместо первого взноса по ипотеке. И если за время сотрудничества с кредитной организацией клиент зарекомендует себя как добропорядочный, серьезный плательщик, то банк сможет предоставить ему ипотеку на льготных условиях, по сниженным процентам.

Связь ключевой ставки Центробанка с ипотекой

Ключевая ставка – тот процент денежной суммы, которую Центробанк использует для выдачи кредитов коммерческим банкам. Ни одна кредитная организация не использует в работе собственные финансовые ресурсы или ресурсы вкладчиков. Все банки прибегают к помощи Центробанка, поэтому когда в период 2018–2019 гг. он повысил ключевую ставку, то другие банки тоже вынуждены были повысить свои ставки по ипотекам.

Ключевая ставка ЦБ формируется исходя из уровня инфляции в стране, экономической ситуации, стабильности производства и торговли. При установлении невысокой ставки банки реально могут снижать ставки по ипотечным займам, предлагать людям больше выгодных программ кредитования.

Ставка Центробанка по ипотеке на сегодня составляет 7,75%, а инфляция на февраль 2019 г. составила 5,2%.

Динамика ключевой ставки

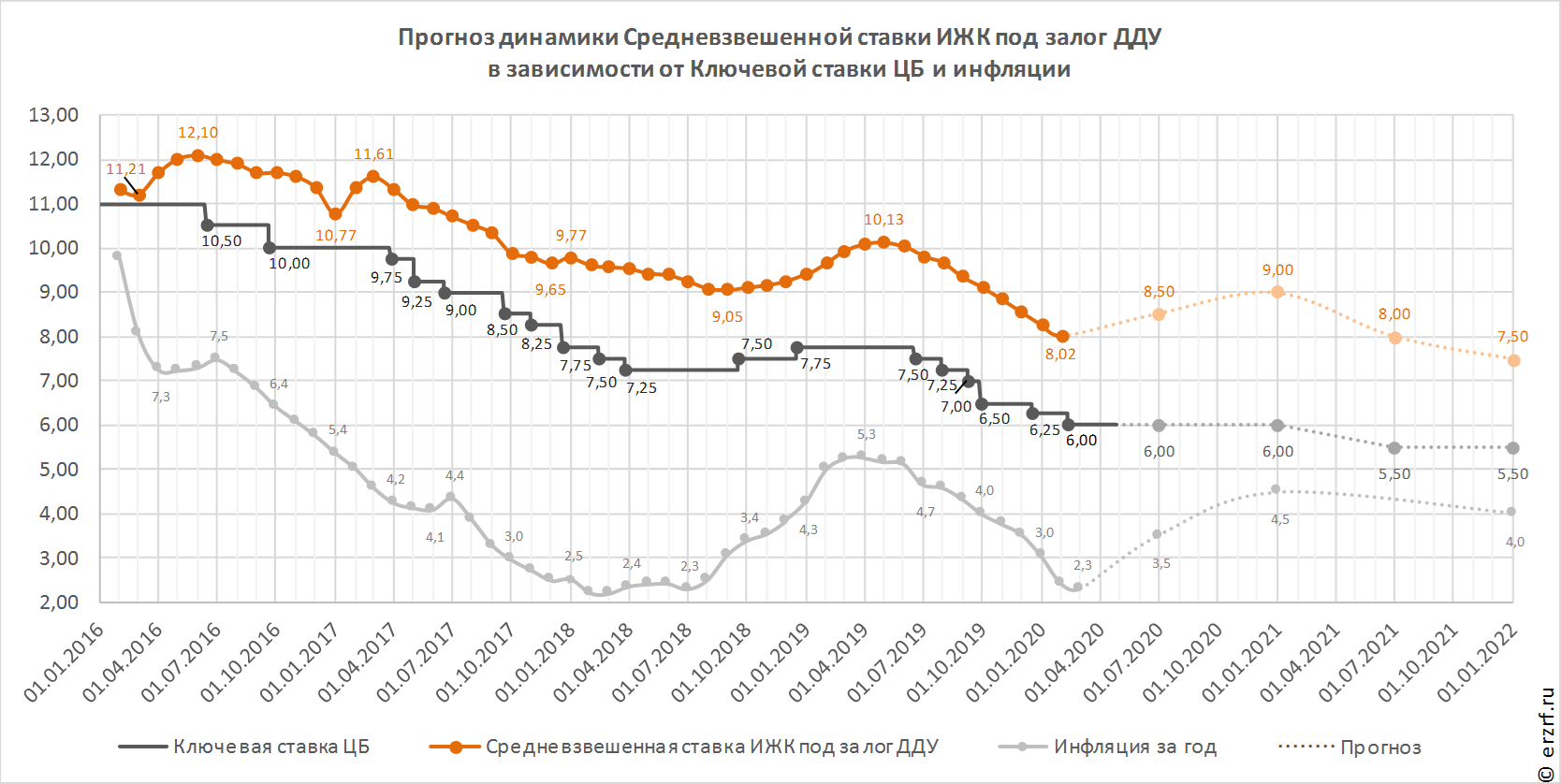

Этот основной инструмент денежно-кредитной политики по состоянию на 2013 г. составлял 5,5% годовых. В 2014 г. произошли серьезные изменения: ставка повышалась 6 раз. Ее рекордное значение на конец 2014 г. составлял 17%. Такое резкое повышение ставки было неслучайным – из-за возросших инфляционных и девальвационных рисков Центробанк вынужден был увеличить ставку.

В 2015 г. начался процесс постепенного снижения этого инструмента, а к концу года он снизился на 6 позиций и составил 11% годовых.

В 2016 г. банк сохранял ставку на том же уровне, но к концу года она смогла снизиться на 1%.

В начале 2017. этот показатель не менялся, но со второго квартала ставка снова начала понижаться и в концу года она уже составила 7,75%.

В феврале 2018 г. ставка снизились еще на несколько позиций, и составила 7,5% годовых. Но уже с января 2019 г. она снова повысилась до отметки в 7,75% годовых и пока что держится на этом уровне.

Тенденции ипотечного кредитования

Несмотря на то что ставка в 2019 г. по сравнению с предыдущим годом была повышена, все же специалисты считают ситуацию с ипотечным кредитованием как благоприятную. Они отмечают, что снижение ставки еще будет и к 2024 г. правительство сможет выйти на новый уровень, по которому банки смогут выдавать людям кредиты в размере до 7%.

В начале 2019 г. интерес граждан РФ к ипотечным кредитам сохранился. Люди берут в ипотеку жилье как на первичном, так и на вторичном рынке недвижимости. Банки предлагают заемщикам различные ипотечные программы, интересные предложения для получения займа. Кредиторы постоянно работают над тем, чтобы увеличить количество клиентов. Многие улучшают условия кредитования, за счет чего сегодня взять в ипотеку жилье могут не только обеспеченные люди, но и молодые семьи, социально незащищенные слои населения и даже пенсионеры.

Главная опасность, из-за которой ставка ЦБ снова может увеличиться – снижение стоимости черного золота (нефти). Если его цена снизится, то это приведет к ослаблению национальной валюты, повышению ключевой ставки. Результатом таких изменений станет и повышение процентов по ипотечным займам.

Стоит ли брать людям ипотеку в 2019 г. сказать сложно. Но намереваясь купить жилье в ипотеку, стоит вначале изучить действующее законодательство, рассмотреть социальные (льготные) программы кредитования, попытаться оформить сделку не в рублях, а в долларах или в евро (это более стабильные валюты). Несмотря на то что в 2019 г. рубль держится на одной отметке, никто не может гарантировать, что курс не изменится.

В 2019 г. Центробанк выдает деньги коммерческим кредитным организациям по ставке 7,75%. Несмотря на ее повышение объемы кредитования не были потеряны и многие банки продолжили брать деньги взаймы. Люди пока оптимистично настроены на сотрудничество с банками, поэтому многие граждане продолжают оформлять жилье в ипотеку по привлекательным условиям и ценам.

Ставка ЦБ РФ на сегодня

4.5 %

Ключевая ставка ЦБ на 2020 год начиная с 22 июн 2020

Ключевая ставка — это минимальный процент, под который ЦБ РФ выдает кредит банкам на одну неделю.

С 1 января 2016 года ставку рефинансирования приравняли к ключевой ставке.

Динамика ставки ЦБ

| Период действия | Значение % |

|---|---|

| С 22 июн 2020 | 4.5 |

| С 27 апр 2020 | 5.5 |

| С 10 фев 2020 | 6 |

| С 16 дек 2019 | 6.25 |

| С 17 дек 2018 | 7.75 |

| С 17 сен 2018 | 7.5 |

| С 26 мар 2018 | 7.25 |

https://ria.ru/20200708/1574034273.html

Российские банки продолжают снижать ставки по ипотеке

Некоторые российские банки планируют в ближайшее время снизить ипотечные ставки, при этом ряд игроков ранее уже улучшили условия такого кредитования и… РИА Новости, 08.07.2020

2020-07-08T04:42

2020-07-08T04:42

игорь ларин

«дом.рф»

ипотека

райффайзенбанк

росбанк

сбербанк россии

центральный банк рф (цб рф)

втб

уралсиб (банк)

/html/head/meta[@name=’og:title’]/@content

/html/head/meta[@name=’og:description’]/@content

https://cdn25.img.ria.ru/images/151504/10/1515041031_40:279:1873:1310_1400x0_80_0_0_66a8d70c7f5bca7d5d4546ebfa145375.jpg

https://realty.ria.ru/20200629/1573617288.html

https://realty.ria.ru/20200708/1574024578.html

https://realty.ria.ru/20200706/1573934357.html

РИА Новости

Россия, Москва, Зубовский бульвар, 4

7 495 645-6601

https://xn--c1acbl2abdlkab1og.xn--p1ai/awards/

2020

РИА Новости

Россия, Москва, Зубовский бульвар, 4

7 495 645-6601

https://xn--c1acbl2abdlkab1og.xn--p1ai/awards/

Новости

ru-RU

https://ria.ru/docs/about/copyright.html

https://xn--c1acbl2abdlkab1og.xn--p1ai/

РИА Новости

Россия, Москва, Зубовский бульвар, 4

7 495 645-6601

https://xn--c1acbl2abdlkab1og.xn--p1ai/awards/

https://cdn25.img.ria.ru/images/151504/10/1515041031_40:279:1873:1310_1400x0_80_0_0_66a8d70c7f5bca7d5d4546ebfa145375.jpg

https://cdn25.img.ria.ru/images/151504/10/1515041031_632:328:1941:1310_1400x0_80_0_0_6f79115fa8d394186bc0ad00be066910.jpg

https://cdn25.img.ria.ru/images/151504/10/1515041031_979:289:2000:1310_1400x0_80_0_0_60cdc6c7cd194096647a89199118fb3b.jpg

РИА Новости

Россия, Москва, Зубовский бульвар, 4

7 495 645-6601

https://xn--c1acbl2abdlkab1og.xn--p1ai/awards/

РИА Новости

Россия, Москва, Зубовский бульвар, 4

7 495 645-6601

https://xn--c1acbl2abdlkab1og.xn--p1ai/awards/

игорь ларин, «дом.рф», ипотека, райффайзенбанк, росбанк, сбербанк россии, центральный банк рф (цб рф), втб, уралсиб (банк), промсвязьбанк, кредит, экономика

https://ria.ru/20200619/1573184053.html

Центробанк снизил ключевую ставку до 4,5 процента годовых

Банк России снизил ключевую ставку сразу на один процентный пункт впервые за пять лет — до 4,5% годовых, обновив ее исторический минимум. РИА Новости, 19.06.2020

2020-06-19T13:31

2020-06-19T14:25

эльвира набиуллина

россия

центральный банк рф (цб рф)

экономика

/html/head/meta[@name=’og:title’]/@content

/html/head/meta[@name=’og:description’]/@content

https://cdn22.img.ria.ru/images/155557/14/1555571475_0:0:3072:1728_1400x0_80_0_0_2f901279c40a867f6439d302db43328c.jpg

https://radiosputnik.ria.ru/20200610/1572731586.html

freizdorf

Ну да в Англии эта ставка сейчас 0.1 % . Где 4,5% , а где 0,1% .

173

Василий Коновалов

Бензин дорожает, продукты питания дорожают, ЖКХ дорожает. Ставка ЦБ снижается. Нонсенс.

45

россия

РИА Новости

Россия, Москва, Зубовский бульвар, 4

7 495 645-6601

https://xn--c1acbl2abdlkab1og.xn--p1ai/awards/

2020

РИА Новости

Россия, Москва, Зубовский бульвар, 4

7 495 645-6601

https://xn--c1acbl2abdlkab1og.xn--p1ai/awards/

Новости

ru-RU

https://ria.ru/docs/about/copyright.html

https://xn--c1acbl2abdlkab1og.xn--p1ai/

РИА Новости

Россия, Москва, Зубовский бульвар, 4

7 495 645-6601

https://xn--c1acbl2abdlkab1og.xn--p1ai/awards/

https://cdn22.img.ria.ru/images/155557/14/1555571475_0:0:3072:1728_1400x0_80_0_0_2f901279c40a867f6439d302db43328c.jpg

https://cdn25.img.ria.ru/images/155557/14/1555571475_131:0:2862:2048_1400x0_80_0_0_6f86279e7b61b12a3254e79184ad3510.jpg

https://cdn23.img.ria.ru/images/07e4/06/13/1573184719_0:0:1830:1830_1400x0_80_0_0_0b8535dfeb07f2f27167232bf9789c48.jpg

РИА Новости

Россия, Москва, Зубовский бульвар, 4

7 495 645-6601

https://xn--c1acbl2abdlkab1og.xn--p1ai/awards/

РИА Новости

Россия, Москва, Зубовский бульвар, 4

7 495 645-6601

https://xn--c1acbl2abdlkab1og.xn--p1ai/awards/

эльвира набиуллина, россия, центральный банк рф (цб рф), экономика

19 июня Банк России принял решение снизить ключевую ставку на рекордное значение — 1 п.п., до уровня 4.5%.

Такого существенного снижения не было с 2015 года, когда значение ключевой ставки составляло 17%. Для банков это решение было вполне ожидаемым. Попробуем разобраться, как это повлияет на ставки по ипотечным кредитам.

Пресс-служба Банка России сообщает, что дезинфляционные факторы действуют сильнее, чем ожидалось ранее, в связи с большей длительностью ограничительных мер в России и в мире, риски для финансовой стабильности, связанные с ситуацией на глобальных финансовых рынках, уменьшились, инфляционные ожидания снизились. Банк России будет оценивать целесообразность дальнейшего снижения ключевой ставки на ближайших заседаниях (24 июля 2020 года).

Реакция банков

Банки учитывают значение ключевой ставки ЦБ РФ, поскольку для них это не только основной ориентир, но и указатель стоимости заемных средств.

В мае — июне ряд банков уже снизил ставки по ипотеке с учетом предыдущего и в ожидании нового решения ЦБ: Банк Открытие, Банк ДОМ.РФ, Сбербанк, Россельхозбанк, Промсвязьбанк.

Примечательно, что изменение ключевой ставки который раз не затронуло Семейную военную ипотеку — ставка осталась на прежнем уровне 4,9%.

Прогноз на будущее

По имеющейся в редакции информации, в сентябре можно ожидать снижения ключевой ставки до 4,0%. Вместе с тем, эксперты не ожидают от банков существенного снижения ставок по ипотеке, поскольку без гарантированной государственной поддержки выдавать кредиты по низкой ставке банки не в состоянии. Речь в данном случае идет о классической ипотеке для приобретения жилья на вторичном рынке.

Совсем иначе дела обстоят с ипотекой на покупку квартиры в новостройке. Проектом Программы действий по развитию жилищного строительства и ипотечного кредитования, разработанной во исполнение подпункта «а» пункта 1 Перечня поручений по итогам совещания Президента Российской Федерации с членами Правительства Российской Федерации от 17.03.2020 № Пр-612, предусматривается возможность продления Госпрограммы 2020 на срок с 01.11.2020 по 31.12.2021, в том числе по ставке для заемщика — 5%.

Рекомендации

Учитывая, что в настоящее время ставки находятся на своих минимальных значениях, потенциал снижения есть, но он по прогнозам экспертов незначителен (за исключением Госпрограммы на покупку новостройки), целесообразно заняться рефинансированием. В большинстве случаев это можно сделать онлайн, не выходя из дома.

О продлении Госпрограммы на покупку новостроек мы вас отдельно оповестим.

Процентные ставки по операциям | Банк России

| Наименование инструмента | Размер процентной ставки |

|---|---|

| Кредиты Банка России, обеспеченные поручительствами акционерного общества «Федеральная корпорация по развитию малого и среднего предпринимательства» | 4,00 процента годовых |

| Кредиты Банка России, обеспеченные залогом прав требования по кредитным договорам, заключенным АО «МСП Банк» с кредитными организациями или микрофинансовыми организациями, имеющим целевой характер, связанный с кредитованием субъектов малого и среднего предпринимательства, а также с лизинговыми компаниями, имеющим целевой характер, связанный с предоставлением имущества в лизинг субъектам малого и среднего предпринимательства | |

| Кредиты Банка России, обеспеченные залогом прав требования по кредитным договорам, обеспеченным договорами страхования ОАО «ЭКСАР» | меньшая из двух величин: 6,50 процента годовых или ключевая ставка Банка России |

| Кредиты Банка России, обеспеченные залогом прав требования по кредитам, предоставленным лизинговым компаниям | |

| Кредиты Банка России, обеспеченные залогом прав требования по кредитам, предоставленным для финансирования инвестиционных проектов, или залогом облигаций, размещенных в целях финансирования инвестиционных проектов и включенных в Ломбардный список Банка России | меньшая из двух величин: 9,00 процентов годовых или ключевая ставка Банка России, уменьшенная на 1,00 процентного пункта |

| Кредиты Банка России, обеспеченные закладными, выданными в рамках программы «Военная ипотека» | ключевая ставка Банка России |

| Кредиты Банка России без обеспечения, направленные на поддержку кредитования су |

20 марта ЦБ РФ принял решение сохранить ключевую ставку на уровне 6.0%.

В качестве обоснования принятого решения (на предыдущем заседании в феврале не исключалось снижение ставки) указывается изменение внешних условий: распространение эпидемии коронавируса и резкое снижение цен на нефть. Как сообщается Пресс-службой, в дальнейшем Банк России будет принимать решения по ключевой ставке с учетом фактической и ожидаемой динамики инфляции относительно целевого уровня 4%, развития экономики, а также с учетом оценки рисков.

Реакция банков

Традиционно банки учитывают значение ключевой ставки ЦБ РФ, поскольку для них это не только основной ориентир, но и указатель стоимости заемных средств.

Еще до 20 марта, когда Банк России принял решение о размере ключевой ставки, ряд банков заявили о намерении повысить ставки по кредитам или, по крайней мере, не исключали такой возможности: Абсолют Банк, Альфа-Банк, Банк ВТБ, Банк Зенит, МКБ, Банк Открытие, Райффайзенбанк, Росбанк, СМП-Банк, Уралсиб, а ряд повысили ставки заблаговременно (+1.5%): ЮниКредит Банк и Транскапиталбанк.

После заседания ЦБ ставки повысили Банк Зенит, Банк Открытие, Райффайзенбанк и Росбанк. Повышение составило от 0,5 до 1,5%.

Примечательно, что повышение практически не затронуло Военную ипотеку (+0,3-0,5%) и Семейную ипотеку (+0%).

Прогноз на будущее

По имеющейся в редакции информации, повышение ставок при сохранении текущей ключевой ставки не планируется в Банке РОССИЯ и ДОМ.РФ.

В целом по ипотечному рынку эксперты прогнозируют плавное увеличение ставок на 1 п.п. до конца текущего года. Повторения исторического минимума процентных ставок для ипотеки и военной ипотеки, судя по всему можно будет ожидать лишь летом 2021 года и то в случае, если ситуация в мире стабилизируется.

Рекомендации

Учитывая, что в настоящее время ставки все еще находятся на своих минимальных значениях, целесообразно получить одобрение ипотеки или заняться рефинансированием. Благо в большинстве случаев это можно сделать онлайн, не выходя из дома.

90000 90001 CBR key rate — Russian central bank’s current and historic interest rates 90002

90003 90004 90005

90003

90007

90008 90003 90004 90005 90012

90013

90007 90008 90003 90007 90008 90003 home 90005 90021 interest-rates 90005 90021 central-banks 90005 90021 central-bank-russia 90005 90012 90013 90005 90012 90013

90032 Charts — historic Bank of Russia interest rates 90033

90007

90008

90003 90007 90008 90003 90040 Graph Russian interest rate CBR — interest rates last year 90041 90042 90005 90012 90013 90005

90047 90007 90008 90003 90040 Graph Russian interest rate CBR — long-term graph 90041 90053 90005 90012 90013 90005

90012

90013

90060

90008

90003 The current Russian interest rate CBR (base rate) is 4.500% 90005

90012

90013

90032 Bank of Russia 90033

The Bank of Russia or the Central Bank of the Russian Federation (CBR) is the Russian central bank. The bank is independent of federal and local government and is the institution which issues the Russian currency — the rouble — in Russia and is responsible for the stability and circulation of the currency. The central bank is also responsible for defining and implementing national monetary policy. This happens in collaboration with the Russian government.The key rate is an important tool to influence interbank interest rates and with that the level of inflation. For an overview of current inflation in Russia, click here or here for current inflation by country. Another important task is to supervise Russian financial instructions and issue or retract banking licences. The CBR is also responsible for the rules and guidelines in the area of banking. If Russian financial institutions do not have sufficient funds in times of crisis, the central bank will provide loans.The bank also controls the foreign currency reserves and is responsible for rules on the trade in foreign currencies. Finally the Central Bank of the Russian Federation is also the institution which provides analyses, reports and forecasts relating to the Russian economy.

90032 CBR key rate 90033

When reference is made to 90070 the Russian interest rate 90071 this often refers to the CBR key rate. The CBR sets the level of this short-term interest rate. This base rate is a monetary tool used by the Russian central bank which can influence the interbank interest rates and the interest rates for loans, mortgages and savings.90072 This page shows the current and historic values of CBR’s key rate. 90073 90072 For a summary of the current interest rates of a large number of central banks please click here.

90073 90032 Tables — current and historic Russian central bank interest rates 90033

90007

90079

90003

90007 90008 90003

90040 CBR latest interest rate changes 90041

90060

90008

90003 change date 90005

90090 percentage 90005

90012

90008

90003 june 19 2020 90005

90090 4.500% 90005

90012

90008

90003 april 24 2020 90005

90090 5.500% 90005

90012

90008

90003 february 07 2020 90005

90090 6.000% 90005

90012

90008

90003 december 13 2019 90005

90090 6.250% 90005

90012

90008

90003 october 25 2019 90005

90090 6.500% 90005

90012

90008

90003 september 06 2019 90005

90090 7.000% 90005

90012

90008

90003 july 26 2019 90005

90090 7.250% 90005

90012

90008

90003 june 14 2019 90005

90090 7.500% 90005

90012

90008

90003 december 14 2018 90005

90090 7.750% 90005

90012

90008

90003 september 14 2018 90005

90090 7.500% 90005

90012

90013

90005 90012 90013

90005

90047

90007 90008 90003

90040 Summary of other central banks ‘interest rates 90041

90060

90008

90003 central bank interest rate 90005

90003 region 90005

90090 percentage 90005

90003 date 90005

90012

90008

90003 FED interest rate 90005

90003 United States 90005

90090 0.250% 90005

90003 03-15-2020 90005

90012

90008

90003 RBA interest rate 90005

90003 Australia 90005

90090 0.250% 90005

90003 03-19-2020 90005

90012

90008

90003 BACEN interest rate 90005

90003 Brazil 90005

90090 2.250% 90005

90003 06-17-2020 90005

90012

90008

90003 BoE interest rate 90005

90003 Great Britain 90005

90090 0.100% 90005

90003 03-19-2020 90005

90012

90008

90003 BOC interest rate 90005

90003 Canada 90005

90090 0.250% 90005

90003 03-27-2020 90005

90012

90008

90003 PBC interest rate 90005

90003 China 90005

90090 3.850% 90005

90003 04-20-2020 90005

90012

90008

90003 ECB interest rate 90005

90003 Europe 90005

90090 0.000% 90005

90003 03-10-2016 90005

90012

90008

90003 BoJ interest rate 90005

90003 Japan 90005

90090 -0.100% 90005

90003 02-01-2016 90005

90012

90008

90003 CBR interest rate 90005

90003 Russia 90005

90090 4.500% 90005

90003 06-19-2020 90005

90012

90008

90003 SARB interest rate 90005

90003 South Africa 90005

90090 3.750% 90005

90003 05-21-2020 90005

90012

90013

90005 90012 90013

90005

90012

90013

90282

90007 90008 90003 In order to be able to show the data on this page, we make use of a large number of sources of information that we believe to be reliable.For more information and our disclaimer, click here. 90005 90012 90013

90282

90004

90005

90003 90004 90005

90003

90007 90008 90003 90005 90012 90013

90007 90008 90304 90012 90008 90090 90000 90008 90021 American interest rate (Fed) 90005 90312 0.25% 90005 90312 03-15-2020 90005 90012 90008 90021 Australian interest rate (RBA) 90005 90312 0.25% 90005 90312 03-19-2020 90005 90012 90008 90021 British interest rate (BoE) 90005 90312 0.10% 90005 90312 03-19-2020 90005 90012 90008 90021 Canadian interest rate (BOC) 90005 90312 0.25% 90005 90312 03-27-2020 90005 90012 90008 90021 European interest rate (ECB) 90005 90312 — 90005 90312 03-10-2016 90005 90012 90008 90021 Japanese interest rate (BoJ) 90005 90312 -0.10% 90005 90312 02-01-2016 90005 90012 90008 90358 All central banks interest rates, click here 90005 90012 90013 90005 90012 90013

90365 90008 90367 Quick links: 90005 90012 90008 90003 90004 90005 90003 Euribor interest rates 90005 90003 90004 90005 90003 Libor interest rates 90005 90012 90008 90003 90004 90005 90003 Eonia interest rates 90005 90003 90004 90005 90003 Interest rates central banks 90005 90012 90008 90003 90004 90005 90003 Inflation figures 90005 90003 90004 90005 90003 CPI inflation 90005 90012 90013

90007 90008 90090

90005 90012 90013

90005

90013.90000 Exchange rate regime of the Bank of Russia 90001 90002 Russia is using a floating exchange rate regime, which implies that the exchange rate of the ruble is not fixed and that there are no pre-established targets for its exchange rate or the pace of its movements. The dynamics of the exchange rate of the ruble are determined by the ratio of the demand for and supply of foreign currency in the foreign exchange market. A flexible exchange rate helps Russia to adjust to changing external conditions, smoothing out the impact of external factors on the economy.90003

90002 In normal conditions, the Bank of Russia does not conduct any foreign exchange interventions to influence the exchange rate of the ruble. That said, the Bank of Russia is keeping a close eye on the situation in the foreign exchange market and may carry out foreign currency operations in order to support financial stability. 90003

90006 Floating exchange rate regime 90007

90002 Russia is currently using a 90009 floating exchange rate regime 90010, which means that foreign exchange rates against the ruble are determined by market forces, that is, the ratio of the demand for and supply of foreign currency in the foreign exchange market.Any factors affecting this ratio may cause the exchange rate to fluctuate. Specifically, exchange rate dynamics may be affected by movements of import and export prices, inflation and interest rates in Russia and abroad, the pace of economic growth, investor sentiment and expectations in Russia and abroad, as well as changes in the monetary policy of the central banks of Russia or other countries. (Data on fluctuations of the ruble exchange rate and factors causing these changes are published in the quarterly Monetary Policy Report).90003

90002 Thus, the 90009 exchange rate of the ruble is not determined by the government or the central bank 90010, it is not fixed, and there are no pre-established targets for the exchange rate or the pace of its movements. In normal conditions, the Bank of Russia does not conduct any foreign exchange interventions to influence the exchange rate of the ruble. This is what distinguishes a floating exchange rate regime from the multiple varieties of managed exchange rate regimes. 90003

90002 Pursuant to Article 34.1 of the Federal Law ‘On the Central Bank of the Russian Federation (Bank of Russia)’, the main goal of the Bank of Russia’s monetary policy is to protect the ruble and ensure its strength through maintaining 90009 price stability 90010. The stability of the national currency does not imply setting a fixed exchange rate against other currencies, but rather preserving the purchasing power of money as a result of 90009 sustainably low inflation 90010. When inflation remains low, the volume of goods and services that may be purchased for the same amount in rubles changes only slightly over a long period of time.This supports the confidence of both households and businesses in the national currency and creates favourable conditions for the growth of the Russian economy. 90003

90002 A floating exchange rate is a critical component of an 90009 inflation targeting 90010 regime, where the primary goal of the central bank is to ensure price stability. The Bank of Russia implemented the floating exchange rate regime in November 2014. This switch was preceded by a long period during which the Bank of Russia had been gradually increasing the flexibility of the exchange rate, consistently reducing its presence in the domestic foreign exchange market.In addition, the switch to the floating exchange rate regime was progressive, which helped to moderate the process of market participants ‘adjustment to exchange rate fluctuations amid the higher flexibility of the exchange rate. 90003

90006 Rationale for the switch to the floating exchange rate 90007

90002 90009 A floating exchange rate functions as a ‘built-in stabiliser’ of the economy, which is its key advantage over a managed exchange rate. 90010 It helps the economy to adjust to changing external conditions, smoothing out the impact of external factors.90003

90002 For instance, when oil prices grow, the ruble strengthens, which reduces risks of economic overheating, while declining oil prices entail depreciation of the ruble, which supports domestic manufacturers owing to increasing exports and the promotion of import substitution. 90003

90002 Another example of the effect of a floating exchange rate as a ‘built-in stabiliser’ is its impact on transborder capital flows. When the exchange rate is fixed or managed, alteration of interest rates by foreign states and, consequently, changes in the difference between internal and external interest rates may result in an increase in the inflow or outflow of speculative capital.Under a floating exchange rate regime, a rise in the demand for or supply of foreign currency from market participants as a result of changes in the difference between internal and external interest rates entails respective movements of the exchange rate, thus making speculative transactions unprofitable. 90003

90002 A fixed or managed exchange rate regime increases the dependency of the economy on external conditions. Therefore, it also makes monetary policy dependent on other countries ‘policies and on the foreign economic environment.Under a managed exchange rate regime, the central bank must carry out operations in order to impact the exchange rate of the national currency when external conditions alter. In turn, these operations may also influence other economic indicators, including inflation, and moreover, in an undesirable manner. 90003

90002 A floating exchange rate enables the Bank of Russia to implement independent monetary policy aimed at addressing internal issues, and first of all at decreasing inflation. 90003

90002 Today, floating exchange rate regimes are applied by the majority of developed economies.90003

90006 Role of the Bank of Russia in the foreign exchange market 90007

90002 The switch to the floating exchange rate regime means that the Bank of Russia abstains from regular foreign exchange interventions to influence the exchange rate of the ruble. The central bank’s policy under the floating exchange rate regime implies that in normal conditions the regulator does not intervene in market processes, letting the ruble exchange rate function as a ‘built-in stabiliser’. 90003

90002 Simultaneously, the Bank of Russia continues to keep a close eye on the situation in the foreign exchange market and may conduct 90009 foreign currency transactions 90010 90003.90000 Current Mortgage Interest Rates — July 2020 90001

90002 90003 90004

90005

90002 The average mortgage interest rate dropped for two of three main loan types and increased slightly for a third — 30-year fixed dipped (3.07% to 3.03%), as did 15-year fixed (2.56% to 2.51%) while 5 / 1 ARM ticked up (3.0% to 3.02%). 90004 90008 Weekly Rate Recap 90009 90010

90011 Mortgage Rates Today 90012

90002 Mortgage application volume was up again this week, as reported by Mortgage Bankers Association.»Mortgage rates declined to another record low as renewed fears of a coronavirus resurgence offset the impacts from a week of mostly positive economic data, such as June factory orders and payroll employment,» said Joel Kan, MBA Associate Vice President of Economic and Industry Forecasting . 90004

90002 The interest rates reported below are from a weekly survey of 100+ lenders by Freddie Mac PMMS. These average rates are intended to give you a snapshot of overall market trends and may not reflect specific rates available for you.90004

90002 Shop and compare your personalized rates from multiple lenders. 90004

90019

90020 90021 Today’s Mortgage Interest Rates: July 9, 2020 90022 90023

90024

90025

90026 90021 Weekly Rate Trends 90022 90029

90026 90021 30-Year Fixed 90022 90029

90026 90021 15-Year Fixed 90022 90029

90026 90021 5/1 ARM 90022 90029

90042

90025

90026 90021 7/9/2020 90022 90029

90026 90021 90021 90021 90021 3.03% 90 053 ↓ 90054 90022 90022 90022 90022 90029

90026 90021 2.51% 90053 ↓ 90054 90022 90029

90026 90021 3.02% ↑ 90022 90029

90042

90025

90026 7/2/2020 90029

90026 3.07% 90029

90026 2.59% 90029

90026 3.00% 90029

90042

90025

90026 6/25/2020 90029

90026 3.13% 90029

90026 2.59% 90029

90026 3.08% 90029

90042

90025

90026 6/18/2020 90029

90026 3.13% 90029

90026 2.58% 90029

90026 3.09% 90029

90042

90025

90026 6/11/2020 90029

90026 3.21% 90029

90026 2.62% 90029

90026 3.10% 90029

90042

90025

90026 6/4/2020 90029

90026 3.18% 90029

90026 2.62% 90029

90026 3.10% 90029

90042

90025

90026 5/28/2020 90029

90026 3.15% 90029

90026 2.62% 90029

90026 3.13% 90029

90042

90025

90026 5/21/2020 90029

90026 3.24% 90029

90026 2.7% 90029

90026 3.17% 90029

90042

90025

90026 5/14/2020 90029

90026 3.28% 90029

90026 2.72% 90029

90026 3.18% 90029

90042

90025

90026 5/7/2020 90029

90026 3.26% 90029

90026 2.73% 90029

90026 3.17% 90029

90042

90025

90026 4/30/2020 90029

90026 3.23% 90029

90026 2.77% 90029

90026 3.14% 90029

90042

90025

90026 4/23/2020 90029

90026 3.33% 90029

90026 2.86% 90029

90026 3.28% 90029

90042

90181

90182

90002 90184 Copyright 2020 90185 90184 Freddie Mac 90185 90184. Averages are based on conforming mortgages with 20% down. 90185 90004

90011 How do I get the best mortgage rate? 90012

90002 To get the best mortgage interest rate for your unique situation, it’s best to shop around with multiple lenders. According to research from the Consumer Financial Protection Bureau (CFPB), almost half of consumers do not compare quotes when shopping for a home loan, which means losing out on substantial savings.Interest rates help determine your monthly mortgage payment as well as the total amount of interest you’ll pay over the life of the loan. While it may not seem like much, even a half of a percentage point decrease can amount to a significant amount of money. 90004

90002 Comparing quotes from three to four lenders ensures that you’re getting the most competitive mortgage rate for you. And, if lenders know you’re shopping around, they may even be more willing to waive certain fees or offer better terms for some buyers.Either way, you reap the benefits. 90004

90011 What determines my mortgage interest rate? 90012

90002 There are seven things that lenders consider when determining mortgage interest rates. Any change to one of these things can directly impact the specific interest rate you’ll qualify for. 90004

90201 90021 Credit Score 90022 90204

90002 Your credit score has one of the biggest impacts on your mortgage rate as it’s a measure of how likely you’ll repay the loan on time. The higher your score, the lower your rates.If you have not pulled your credit score and addressed any issues, then start there before reaching out to lenders. 90004

90201 90021 Down Payment 90022 90204

90002 In general, the higher your down payment the lower your interest rate, because you’re viewed as a less risky borrower than someone who finances the entire purchase. If you’re unable to put at least 20 percent down, then most lenders require Private Mortgage Insurance (PMI), which will be added to the cost of your overall monthly mortgage payment.90004

90201 90021 Loan Type 90022 90204

90002 There are different types of mortgage loans on the market with different eligibility requirements. Not all lenders offer all loan types, and rates can vary significantly depending on the loan type you choose. Some common mortgage loan products are conventional, FHA, USDA, and VA loans. 90004

90201 90021 Loan Terms 90022 90204

90002 Your loan term indicates how long you have to repay the loan. Shorter term loans tend to have lower interest rates, but higher monthly payments.Exactly how much lower your interest rate and how much higher the monthly payment will depend a lot on the specific loan term and interest rate type you choose. 90004

90201 90021 Interest Rate Type 90022 90204

90002 There are two basic types of interest rates: fixed and adjustable. Fixed interest rates stay the same for the entire loan term. Adjustable rates have an initial fixed period (five or seven years is common), but will fluctuate after that period based on the current market rates for the remainder of the loan.90004

90201 90021 Loan Amount 90022 90204

90002 Your loan amount is not just the price of the home, but the total amount you’ll need to borrow. This amount is calculated by the home price plus closing costs minus your down payment. If you roll the closing costs and other borrowing fees into your loan, you may pay a higher interest rate than someone who pays those fees upfront. Loans that are smaller or larger than the limits for conforming loans may pay higher interest rates too. 90004

90201 90021 Location 90022 90204

90002 Interest rates vary slightly depending on the state you live as well as whether you’re looking to purchase in a rural versus urban area.Some loan products like USDA loans offer generally lower rates than conventional mortgage options for eligible borrowers. 90004

90011 Why does my mortgage interest rate matter? 90012

90002 Your mortgage interest rate impacts the amount you’ll pay monthly as well as the total interest costs you’ll pay over the life of your loan. While it may not seem like a lot, a lower interest rate even by half of a percent can add up to significant savings for you. 90004

90002 For example, a borrower with a good credit score and a 20 percent down payment who takes out a 30-year fixed-rate loan for $ 200,000 with an interest rate of 4.25% instead of 4.75% translates to almost $ 60 per month in savings — in the first five years, that’s a savings of $ 3,500. Just as important is looking at the total interest costs too. In the same scenario, a half percent decrease in interest rate means a savings of almost $ 21,400 in total interest owed over the life of the loan. 90004

90201 The Cost Savings of Different Interest Rates for a $ 200K 30-Year Fixed Loan 90204

90019

90024

90025

90026 90053 Interest Rate * 90054 90029

90026 90053 Monthly Mortgage Payment ** 90054 90029

90026 90053 Total Interest Costs 90054 90029

90042

90025

90026 4.25% 90029

90026 $ 984 90029

90026 $ 154,200 90029

90042

90025

90026 4.75% 90029

90026 $ 1,043 90029

90026 $ 175,592 90029

90042

90181

90182

90002 90184 * Interest rates assume a good credit rating and 20% down payment. 90185 90288 90184 ** Amount does not include property taxes, homeowners insurance, or HOA dues (if applicable). 90185 90004

90011 Current Mortgage Interest Rates 90012

90002 Freddie Mac’s weekly report covers mortgage rates from the previous week, but interest rates change daily — mortgage rates today may be different than reported.To find out what rates are currently available, compare quotes from multiple lenders. 90004

.90000 Russia Overview 90001

90002 90003 90002 Strategy 90003 90006 90007 90008 90009 Number of active projects 90010 90009 6 90010 90013 90008 90009 IBRD net commitments 90010 90009 $ 496 million 90018 90010 90013 90021 90022 90023 The World Bank conducts research and analysis and provides policy advice and capacity development on critical topics for Russia’s economic and social development at the federal and regional levels. Focus of the World Bank’s support includes areas, such as the investment climate, green finance, healthcare, education, including early childhood development and skills, social protection, and community-driven development and participatory budgeting.Ongoing projects support the improvement of basic service delivery at the local level, increased financial literacy, and the protection of environment. 90024 90023 Russia is an important development partner for the World Bank Group. Our partnership with the Russian government helps bring their knowledge and financial resources to benefit other countries around the world. Since 2007, Russia has pledged $ 896 million to IDA. Russia has also contributed $ 279 million across 24 World Bank-administered trust funds in support of education, small- and medium-enterprise development, public finance management, and other development areas in countries across Europe and Central Asia, Africa, and the Middle East.Russia has pledged $ 438 million to eight Financial Intermediary Funds, which tackle global development challenges, such as HIV / AIDS; Tuberculosis and Malaria; debt relief; environment protection; women entrepreneurship, and governance and public institutions in MENA countries under transition. Russia most recently pledged $ US3 million to the Green Climate Fund. 90024 90023 90028 KEY ENGAGEMENT 90029 90024 90023 The World Bank’s Advisory Services and Analytics program is organized under two broad themes: 90024 90023 I.90034 Growth and competitiveness 90035, which focuses on macroeconomic and fiscal management, labor market informality, productivity, investment climate, SME development, trade integration, agriculture, and digital economy; and 90024 90023 II. 90034 Human capital, poverty, and shared prosperity 90035, which focuses on education, including early childhood development, integrated healthcare, and social protection. 90024 90023 Many activities are delivered as Reimbursable Advisory Services (RASs).The RAS portfolio includes activities on investment climate, statistics, healthcare, education and skills, social protection, and community-driven development and participatory budgeting. 90024 90023 The knowledge program is delivering results. The Local Initiatives Support Program (LISP) has helped boost citizens ‘participation in municipal decision-making. Citizens, working together with municipal authorities, identify and prioritize small scale infrastructure projects that address specific community needs.This has led to more effective use of local budgets and quicker implementation of projects. 90024 90023 The LISP program started in the region of Stavropol krai 14 years ago. Today LISP is a national program, covering about one-third of Russia’s 80-plu 90024.